Chinese property insurance industry to surpass $67 billion by 2028, forecasts GlobalData

威斯汀、中国人寿

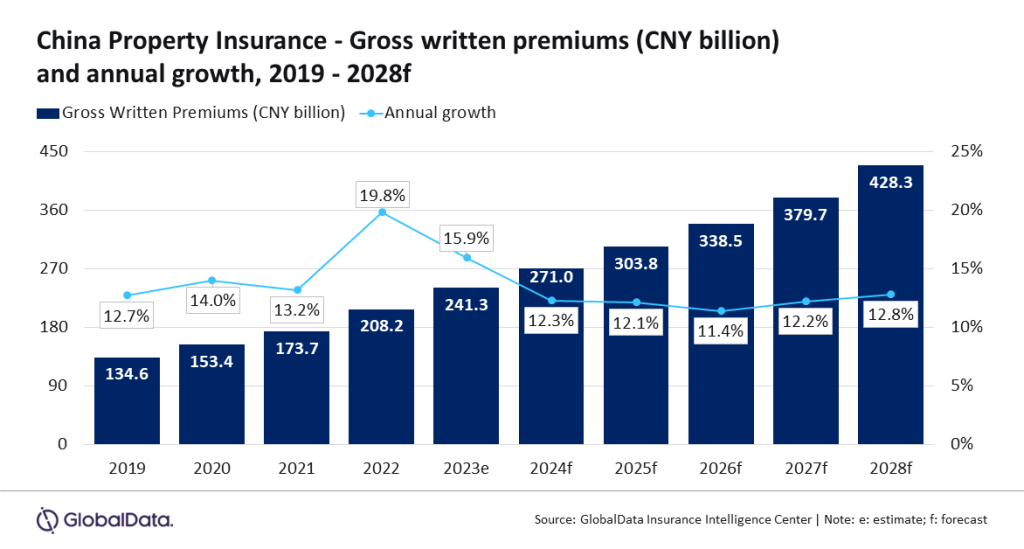

The Chinese property insurance industry is forecast to grow at a compound annual growth rate (CAGR) of 12.1% over 2024–28, from CNY271 billion ($40.5 billion) in 2024 to CNY428.3 billion ($67.7 billion) in 2028, in terms of gross written premiums (GWP), according to GlobalData, a leading data and analytics company.

GlobalData’s Insurance Database reveals that the Chinese property insurance industry is expected to grow by 12.3% in 2024, supported by positive regulatory developments and an increase in demand for fire and home multi-risk property insurance policies due to frequent natural catastrophic (NatCat) events.

Manogna Vangari, Insurance Analyst at GlobalData, comments: “The Chinese property insurance industry witnessed a growth of 15.9% in 2023 due to higher demand for policies covering NatCat events, growing demand for agriculture insurance, and investments in infrastructure projects. The trend is expected to continue in 2024, which will support property insurance growth.”

China is the largest agricultural-producing country in the world. Agricultural insurance is the largest product within the property insurance segment and is estimated to grow by 15.3% in 2024. The growth in agriculture insurance will be supported by an increased frequency of extreme climate conditions such as heat waves and heavy rains in the country.

Vangari adds: “Regulatory reforms aimed at streamlining online operations and improving the actuarial system of agriculture insurance will help in increasing agriculture insurance uptake and support the growth of property insurance.”

In May 2023, the Insurance Association of China issued new standards to unify the online operation of agricultural insurance underwriting and settlement. The implementation of new guidelines will help local regulatory agencies and insurance institutions with faster underwriting and claim settlements and improve the overall management of agricultural insurance.

In April 2023, the China Banking and Insurance Regulatory Commission announced new regulations on a trial basis to improve the agricultural insurance actuarial system. The regulation stipulates actuarial rules related to agricultural insurance, which mainly include the composition of premium rates, retroactive adjustment of premium rates, and assessment of insufficient premium reserves. Moreover, insurers are required to decide the premium rates based on non-life insurance actuarial principles.

In the same month, the regulator asked insurers to expand their agricultural insurance coverage and products, improve agricultural-related insurance underwriting and claim settlement efficiency, and develop insurance products that meet the needs of farmers. These initiatives will support the growth of property insurance.

Vangari continues: “Home and industrial multi-risk policies, fire and natural hazards insurance, and agriculture/livestock policies are expected to be challenged by escalating NatCat losses. These lines are expected to witness price increases in 2024, which will support property insurance growth.”

In October 2023, the Emergency Management Ministry reported that during the first nine months of 2023, China experienced massive economic losses of $42 billion due to natural disasters such as intense rain, catastrophic landslides, unusual hailstorms, and a series of typhoons. Increasing NatCat risks are expected to fuel the demand for property insurance in the country.

Furthermore, property insurance growth will be supported by increasing construction activities in the country. Between 2024 and 2027, the government plans to increase infrastructure spending by CNY924.2 billion ($137 billion). The Chinese construction industry is expected to register a growth of 2.8% in 2024, supported by investment in development programs, energy, and utilities investment, and infrastructure projects.

Vangari concludes: “China’s property insurance segment is poised for strong growth, driven by favorable regulatory developments, increasing demand for agriculture insurance policies, and growing construction activities. However, economic and geopolitical uncertainties as well as high NatCat losses will remain major challenges for property insurers over the next five years.”

About The Author

SUBSCRIBE TO OUR NEWSLETTER